The Global Infrastructure BoomThe next 20 years will see an unprecedented global investment in infrastructure. Two primary factors will fuel this boom:

1. The aging of the infrastructure in the developed world.

2. Economic growth, especially in the developing world.

New and better infrastructure will be needed everywhere, not because it is an end unto itself, but because it provides the means for people to realize radically improved lifestyles.

In short, infrastructure will drive prosperity and growth, which will have a positive impact on quality of life globally. This includes social well-being, health, and safety of citizens.

The primary challenges will lie in funding these enormous investments and ensuring that the resources are not mis-allocated to fund ābridges to nowhereā and āgreen projectsā that deliver no real payback.

This surge in spending is necessary because the long-term economic well-being of both emerging and developed economies is threatened by the infrastructure gap caused by years of under-investment, as well as mal-investment. The fact is, existing infrastructure will not be adequate to meet the demands of the economic growth to come.

This is especially true in the developing world, where transportation and other types of infrastructure were never built to serve even todayās increasingly urban population.

For instance, meeting the needs of the population and expected economic activity of 2030 means that transportation infrastructure will need to handle two to three times as many passengers as it does today.

According to the Futures Project on Transcontinental Infrastructure from the Organization of Economic Cooperation and Development (OECD), between now and 2030:

- Airline traffic worldwide will grow by 4.7 percent per year.

- Airfreight will increase by around 5.9 percent annually.

- Maritime container traffic will increase by more than 6 percent per year.

- Railroad passenger traffic will increase around 2 percent annually.

- Railroad freight traffic worldwide could increase at around 3 percent per annum.

As a result, air passenger traffic could double in just 15 years, air freight could triple in 20 years, and port handing of maritime containers worldwide could quadruple by 2030.1

Since the current infrastructure wonāt be able to handle even a 50 percent increase, we must act quickly to ensure that growth is not stymied by this looming infrastructure bottleneck.

Thatās why the success of the coming global economic revolution depends as much on solid planning and unencumbered free markets as it does on breakthrough technologies and healthy demographics.

Because of current deficit and debt levels in most countries, plodding government-funded infrastructure projects will need to be replaced or enhanced by improved funding and financing arrangements enabled by the private sector.2

Putting the right infrastructure, in the right places, at the right time, to maximize global quality of life is not a simple matter. It impacts virtually every economic sector and differs dramatically from country to country.

More importantly, long lead-times mean that planners who wait for crises, like the ones we see in Mumbai or Calcutta, risk creating human suffering and not realizing the full potential of economic growth. However, itās also a big risk when countries invest too far ahead, as China may have done with its āghost citiesā and āhigh-speed railroads to nowhere.ā

That why itās necessary to study the trajectory of growth; anticipate the needed infrastructure; and create incentives that encourage both the public and private sectors to place optimal bets on infrastructure.

So, what do these needs look like today? Consider these facts:

Demand for energy, especially electricity, will increase greatly between now and 2030. Already, demand for electricity is increasing twice as fast as overall energy use.3

Over the next 20 years or so, this strong growth will be driven not only by population growth, but by rising standards of living in developing countries. The result: a very rapid increase in electricity service, particularly in the developing world.

Conservative estimates by the OECD predict that global electricity demand will grow at an average of 2.5 percent per year; thatās a cumulative 76 percent by 2030. Asia is expected to have the most dramatic increase, averaging 4.7 percent per year. Much of this growth will come from connecting the roughly two billion people worldwide who currently lack electrical power.

Today, the worldās electrical power generation breaks down as follows:

- Coal: 40 percent

- Natural gas: 21 percent

- Hydroelectric and other renewable: 20 percent

- Nuclear: 14 percent

- Other sources: 5 percent

The future structure of electrical power generation will be determined by several factors, including:

- New developments in technology

- Relative cost of fuels and capital equipment

- Upheavals in international energy markets

The World Energy Outlook 2011 āNew Policies Scenarioā4 projects that nuclear power capacity will increase by 60 percent by the year 2035. Because of its reliability, it will increasingly be chosen for the growing large-scale, base-load electricity demands. Other factors affecting this choice will include:

- Fear of climate change

- Concerns over the security of the energy supply

- Evolving economic realities, including the relative cost of fossil fuels versus enriched uranium, thorium, and depleted uranium

Notably, the infrastructure challenge related to electrical distribution is likely to be more difficult to deal with than the shortfall in generating capacity. From this perspective, antiquated North American and EU infrastructure may be as much of a liability as the non-existent infrastructure in much of India and China.

Like electricity, fresh water will be a major element driving quality of life and economic growth. Already, except for Europe, Russia, and most of North America, water resources are being stressed by decreasing water availability and declining water quality.

For this reason, research is underway in many places to seek solutions. New technologies, policies, and practices for delivering water and disposing of waste are rapidly emerging.

These solutions are being implemented as aging water systems are upgraded with the infrastructure needed for extracting, collecting, treating, testing, and distributing water. However, compared to other utilities, water services need more capital.

For example, a water utility requires twice as much upfront investment as an electrical utility with the same annual operating expenses. So, in order to guarantee the flow of potable water from the tap, maintain the water infrastructure in tip-top shape, and increase the availability of water to under-served areas, the issue of financing will need to be addressed.

Over the next three decades, the global demand for passenger rail services and related infrastructure will also grow. This demand will be driven by underlying economic and demographic forces, including:

- Highway congestion

- Highway safety

- National security

- Environmental concerns

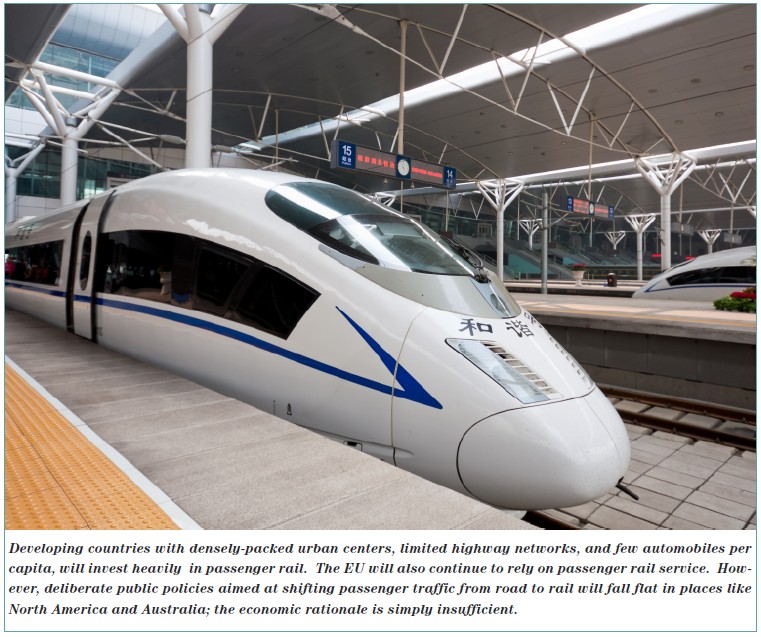

In developing countries with densely packed urban centers, limited highway networks, and few automobiles per capita, passenger rail is an obvious choice. The EU will also continue to rely on passenger rail service.

However, deliberate public policies aimed at shifting passenger traffic from road to rail will fall flat in places like North America and Australia; the economic rationale is simply insufficient.

However, even those places will see a shift from road to rail for freight, as supply-chain optimization makes the advantages of rail clear.

Many of the worldās railroad infrastructure projects will be large āmegaprojects.ā These projects will likely require Public-Private Partnerships because of their scope.

They will not only be seen as investments and revenue generators; they will impact virtually all areas in society, playing a role in poverty reduction, regional development, and environmental and cultural preservation.

Urban public transportation has traditionally aimed at meeting the needs of city-bound, low-income users. For a time, this segment experienced a decline due to the rise in use of private cars, and the drain on public funds caused by investment needs and operating subsidies.

But now, based on projected needs looking out to 2030, many large cities are increasing their investment in urban public transportation. This is happening in both the industrialized world and in emerging countries such as Brazil, China, and India.

Among the factors that will encourage more public transportation will be increased travel times, rising gasoline prices, and rising costs of parking and tolls.

To meet this growing need, the capital investment needs will be enormous. In some countries, systems will be built and maintained solely by public monies. In others, competition and private initiatives will be employed.

A key national asset for any country is its road infrastructure. It fosters the free movement of people and helps drive a ācommon market.ā Where roads are inadequate, as in Columbia and Pakistan, there is frequently rural poverty, political instability, and difficulties in providing relief from famine and floods.

In the coming decades, the biggest additions in road infrastructure will be made in developing countries such as China and India, which have concluded that a national expressway network is needed to create a modern economy. China is on a path to achieve this goal in 20 years, with India not far behind.

In developed countries, the OECD forecasts that traffic congestion will continue to increase as roads will become overwhelmed by too many vehicles. However, shifting freight from trucks to trains, self-driving cars, and increased telecommuting will all help to minimize this congestion.

Nevertheless, a lag between demand and supply is inevitable as long as roads are publicly funded. In the coming years, there will be more Public-Private Partnerships, but the ROI is too small and risky for purely private funding of roadways.

Demand for telecommunications services will, of course, be driven by growing populations, but it will be the expansion of the middle-class around the globe and their move into a connected lifestyle that will accelerate the expansion of bandwidth. The proliferation of telecommuting will also add greatly to demand.

Telecom infrastructure investments will total between $10 trillion and $15 trillion through 2030. The funding and growth of telecom will be significantly different than other infrastructures for the key reason that this sector will continue to be almost exclusively supported by the private sector.

Private ownership, plus low barriers to entry, will help maximize the power of competition that will strengthen the industry. Unlike most other types of infrastructure:

- Demand will be managed through pricing.

- Third-party access will infuse growth into the system.

- The strong framework that competition creates will contend well with the challenges of ever-expanding regulations.

Based on this trend, we offer the following forecasts:

First, investment in infrastructure between 2010 and 2030 will total between $70 trillion and $100 trillion.

Itās almost certain that by 2030 the global population will grow to 8 billion from todayās 7 billion. The $70 trillion estimate assumes global GDP growing to $150 trillion from $82.8 trillion today. Under this scenario, the U.S. represents about 19 percent of global GDP today, and somewhere around 15 percent in 2030. These numbers are based on an improbably low growth rate for the U.S. of about 2 percent per year, and a 3.4 percent rate for the global economy. Given that weāre entering the deployment phase of the current techno-economic revolution, the Trends editors expect to see global GDP grow to $208 trillion by 2030. Under this scenario, the United States will grow at a 3.7 percent annual rate, while China will grow at an 8 percent rate. Assuming that infrastructure needs to grow in direct proportion to a rise in real GDP, the low-end $70 trillion cumulative infrastructure investment estimate should be revised to a much more realistic forecast of $100 trillion.

Second, this infrastructure investment will require innovative funding mechanisms.

The current economic crisis has reduced the public funds available for infrastructure investment, which simply continues a 30-year decline relative to GDP. In addition, traditional sources of private financing have also become severely limited, while commercial banks face their own capital and liquidity constraints. Consequently, new approaches to financing will need to be mobilized.5 The Trends editors foresee at least four developments:

- Public-Private Partnerships will increasingly be relied upon for securing financing and diversifying business models.

- Incentives will be increased for pension funds and other large institutional investors to invest in infrastructure.

- User charges will be increased as a means for capturing funding and letting market forces drive investment priorities.

- Land value capture will be leveraged as a source of funding.

Third, investment in infrastructure will provide badly needed job opportunities for the 1.2 billion people around the world who are currently under-employed.

This impact will be felt in two ways:

- The direct employment of workers for infrastructure projects will be significant.

- An even larger impact will come from enabling whole new industries, which will put cash purchasing power in the hands of consumers who will then demand a wider range of goods and services. Across the globe, a new consumer middle class will arise, looking to improve its standards of living.

Fourth, telecom infrastructure investments will overwhelmingly occur in the developing world and, unlike other investments, they will be heavily front-loaded.

Whether weāre talking about cell towers or fiber links, once the big initial investment is made, it can be repeatedly refreshed using newer technologies that offer much higher capabilities for much lower costs. Countries that still lack basic upgradeable infrastructure will warrant heavy investment in the next 5 to 10 years and reduced investment beyond that.

References List :

1. BusinessWire, April 11, 2012, "$53 Trilion in Infrastructure Needed by 2030 ? OECD/Oliver Wyman." ā Copyright 2012 by BusinessWire, a Berkshire Hathaway Company. All rights reserved. http:/ businesswire.com 2. For insights into infrastructure investing, visit the Altius Associates website at: http://www.altius-associates.com 3. For more information about increased electricity demand in the next 20 years, visit the World Nuclear Association website at: http://www.world-nuclear.org 4. AOL Government, April 20, 2012, "Rethinking Infrastructure Funding," by Ed Crooks and Michelle Quadt. ā Copyright 2012 by AOL Inc. All rights reserved. http://gov.aol.com 5. For additional insight into the World Energy Outlook 2011, visit the World Energy Outlook/International Energy Agency website at: http://www.worldenergyoutlook.org